Boosting your profit margins isn't just about selling more; it's about earning more from what you already sell. The smartest way to do this is by both increasing your revenue and tightening your control over costs. This means you need to get strategic with your pricing, rein in operational spending, and make your entire business run more efficiently. It's about looking past the top-line sales number and digging into the profitability of every single sale.

First, Get a Clear Picture of Your Current Profit Margins

Before you can start making improvements, you need to know exactly where you stand. Think of it like a doctor running diagnostics before writing a prescription. You have to understand your business's financial health right now to have any hope of making it stronger. This is the essential first step.

This initial deep-dive isn't about getting lost in complex accounting. It’s about getting to grips with three core metrics that, together, tell the real story of your business's performance.

Your Quick Guide to Profit Margin Types

To really understand where your money is going, you need to be familiar with the three main types of profit margins. Each one offers a different lens through which to view your business's financial performance. Here’s a quick breakdown to get you started.

Understanding these distinctions is crucial. They are your financial diagnostic tools.

Why Each of These Margins Tells a Different Story

Each margin gives you a unique piece of the puzzle. For example, you might have a fantastic gross margin, which means your product itself is selling for a healthy profit. But if your net margin is razor-thin, it’s a massive red flag. It tells you that your operational costs—things like rent, marketing spend, or administrative salaries—are chewing up all your profits.

This kind of insight is gold. It helps you pinpoint the exact area of the business that needs attention. Instead of guessing, you can act with precision.

If you want to get hands-on with your own numbers, it's well worth your time to master margin calculations in Excel. Being able to confidently translate your raw data into actionable insights is a game-changing skill for any business owner.

Knowing your numbers is more important than ever. Consider this: UK corporate profits hit an all-time high of £156,359 million in the first quarter of 2023, showing just how much opportunity is out there. To get your slice of that pie, you need to have a rock-solid understanding of your own financial performance.

By dissecting these three key margins, you move from simply knowing your revenue to truly understanding your profitability. This foundational knowledge is what separates businesses that merely survive from those that genuinely thrive.

Mastering Pricing to Boost Your Bottom Line

Your pricing strategy is the single most powerful tool you have for improving profit margins. Too many businesses get stuck in the rut of simple cost-plus pricing, but honestly, that approach often leaves a staggering amount of money on the table. It completely ignores the real value your customers get from what you do.

Let's move beyond that basic formula and explore smarter pricing that directly fattens up your bottom line.

Rethinking your pricing isn’t about just hiking up your costs for the sake of it. It’s about getting your prices in sync with the immense value you deliver. Once you make that mental shift, you gain the confidence to make changes that create immediate and lasting profit growth.

This isn't just theory; it's a strategy that many UK firms have been quietly using for years. A deep dive into company balance sheets shows a steady climb in markups since 2014, with a significant jump over the last decade. This trend isn't just about market shifts—it's driven by firms deliberately raising prices, showing they recognise pricing power as a key profit lever. You can see the data yourself in these findings on UK firm markups.

Adopt a Value-Based Pricing Model

Stop asking, "What does this cost me to make?" Instead, start asking, "What problem does this solve for my customer, and what is that solution actually worth to them?" That question is the very heart of value-based pricing.

Imagine you run a software company with a slick project management tool. A cost-plus model might lead you to price it at £50 a month, based on your development and support overheads.

But what if that tool saves your average client 10 hours of tedious admin time every single month? And what if their team's time is valued at £40 per hour? You're not just selling software; you're delivering £400 of tangible value. Suddenly, a price of £150 per month doesn't just feel fair—it feels like an absolute bargain for the client.

To get this right, you need to get inside your customers' heads and quantify the benefits you provide.

- Talk to your best customers: Interview them and ask what specific results they've seen since using your product or service.

- Build powerful case studies: Document the concrete return on investment (ROI) your clients are achieving.

- Survey your target market: Get a feel for their perceived value of the solutions you offer before they even sign up.

Introduce Tiered Pricing Options

Let's face it, one price rarely fits all. Tiered pricing is a brilliant way to cater to different segments of your customer base, which helps you maximise revenue from each one. By offering a few distinct packages, you give people a choice and gently guide them toward the option that best fits their needs and budget.

Take a digital marketing agency offering SEO services. Instead of a single flat fee, they could structure their offering like this:

This structure is a game-changer. It stops you from undercharging larger clients who need more resources while keeping an accessible entry point for the little guys. It puts the power of choice in the customer's hands.

Analyse Competitors Without Starting a Price War

Knowing what your competitors charge is vital, but it should only be one data point, not the sole dictator of your own prices. The goal is to understand the market, not to blindly copy the cheapest price you can find.

A race to the bottom is a battle nobody wins—it just torches margins for the entire industry. Your real objective is to position your offering based on its unique value, not just its price tag.

If a competitor is significantly cheaper, dig in and find out why. Are they offering fewer features? Is their customer support notoriously flaky? Use these differences to justify your higher price point.

You need to clearly communicate your unique selling proposition (USP). If you offer superior quality, faster delivery, or exceptional service, make sure your marketing and sales conversations hammer these points home. This single-handedly shifts the conversation from price to value.

For more practical ideas on boosting your financial performance, check out our comprehensive guide on how to increase profit margins. By positioning yourself strategically, you can command a premium price and protect your profitability for the long haul.

Cutting Costs Without Compromising on Quality

Slashing your expenses is often the quickest way to pump up your profit margins. After all, every single pound you save goes directly to your bottom line. But this isn't about taking a sledgehammer to your budget. A clumsy approach can easily damage the quality of your product, frustrate your customers, and sink team morale.

The real skill lies in making smart, strategic cuts that get rid of waste without sacrificing the very things that make your business special. It’s about becoming leaner and more efficient, not just cheaper.

This whole process has to start with a deep dive into every single one of your expenses. You'd be surprised what you find when you look closely—those small, recurring costs can add up to a shocking amount over the course of a year. The mission is to hunt down non-essential spending that you can trim without anyone even noticing.

Get Forensic with a Spending Audit

Before you can cut anything, you need a painfully clear picture of where your money is actually going. This means grabbing your accounts and going through them with a fine-tooth comb, categorising every single expense. I’m talking everything, from major overheads like rent right down to the smallest software subscription.

This kind of detailed review almost always uncovers some quick wins. For instance, you might discover you're still paying for software licences for people who left the company months ago, or for tools the team has long since abandoned. These are what I call 'zombie subscriptions', and they're quietly siphoning cash out of your business every single month.

Once you have your complete list, it’s time to play detective with each line item:

- Is this absolutely essential? Does it directly help bring in revenue, keep customers happy, or is it a non-negotiable operational need?

- Is there a better value alternative? Could you get a similar result from another supplier or a different piece of software for less money?

- Can we negotiate this down? Are you on the best plan for your current needs, or is there some wiggle room on the terms?

Going through this meticulous process gives you the data you need to make informed, confident decisions instead of just reacting. If you want to go deeper on this, you can find more actionable ideas to cut business expenses without stunting your growth.

Don't Be Afraid to Renegotiate with Suppliers

Your relationships with suppliers should feel more like partnerships than just simple transactions. If you’ve been a loyal customer for a while, you have more leverage than you probably realise. It’s time to use it. Don't shy away from starting a conversation about your current terms.

A good starting point is to do a bit of research. Find out what your competitors are paying for similar goods or services to get a benchmark. Then, approach your key suppliers with a clear goal in mind. You could offer to sign a longer-term contract in exchange for a better price, or perhaps ask for a loyalty discount based on your solid payment history.

A simple phone call can often lead to some pretty significant savings. Most suppliers would much rather offer a modest discount than risk losing a reliable, long-term client. The key is to be respectful and frame it as a win-win.

And this doesn't just apply to your material suppliers. You can negotiate with your landlord, your insurance provider, and even your software vendors. Every pound saved from a successful negotiation is a direct boost to your profit margin.

Embrace Lean Thinking to Eliminate Waste

Beyond the obvious costs, operational waste is a silent killer of profit. Lean principles, which originally came from the world of manufacturing, are all about systematically stamping out any activity that doesn't add real value for your customer. The great thing is, this concept works for any type of business, whether you're a creative agency or a tech start-up.

Think about the parts of your business where time or resources just seem to vanish. This could be clunky workflows that force people to enter the same data twice, too much stock tying up cash, or time wasted fixing mistakes that shouldn't have happened in the first place.

Here are a few common culprits to look out for:

- Overproduction: Creating more of a product or service than people are actually buying.

- Waiting: Dead time when people or processes are just sitting idle, waiting for the next step.

- Unnecessary Motion: Employees wasting movement on tasks that don't add any value.

- Defects: The very real cost of rework, repairs, and fixing errors.

By building a culture where every single person on your team is encouraged to spot and suggest ways to reduce waste, you create efficiency that lasts. This turns cost-cutting from a top-down order into a collaborative team effort, making your business genuinely stronger, not just cheaper.

Driving Profit Through Operational Efficiency

Think of your business's day-to-day operations as its engine. A well-oiled machine not only performs better but is also far more fuel-efficient, which has a direct impact on your bottom line. Refining how your business runs is one of the most reliable ways to widen your profit margins because it hits both sides of the financial equation: you cut costs while freeing up resources to chase more revenue.

It really boils down to creating smarter, smoother workflows that get more done with less wasted time and money. For a lot of UK businesses, this is make-or-break stuff. The median profit for SMEs in 2023 hovered around £13,000. While some sectors, like property services, saw figures closer to £15,000, many in retail and manufacturing were averaging just £11,000. It's a stark reminder of just how tight the margins can be.

Those numbers really drive home how crucial it is to squeeze every last drop of value from your operations.

Automate the Repetitive Grind

Take a moment and think: how much time does your team really spend on manual, repetitive tasks each week? Things like data entry, chasing invoices, or pulling the same old reports are necessary evils, but they don't add direct value. Worse, they’re a prime source of human error and can be a real drain on morale.

This is where automation can be a game-changer. Using some fairly simple software tools, you can put these administrative chores on autopilot.

- Financial Admin: Let your accounting software automatically send out invoice reminders or categorise expenses.

- Customer Comms: Set up automated email sequences to welcome new clients or follow up on initial enquiries.

- Internal Workflows: Use project management tools to automatically assign the next task in a sequence and notify the relevant team member.

The aim here isn't to replace your people but to liberate them from the tedious stuff. This gives them the headspace to focus on high-value work like brilliant customer service, strategic thinking, and innovation—the activities that actually fuel growth.

Fine-Tune Your Supply Chain and Stock

Your supply chain and inventory management are often hiding some of the biggest opportunities for cost savings. Holding too much stock ties up cash that could be working for you elsewhere. On the other hand, holding too little puts you at risk of stockouts and frustrated customers. The real art is in finding that perfect balance.

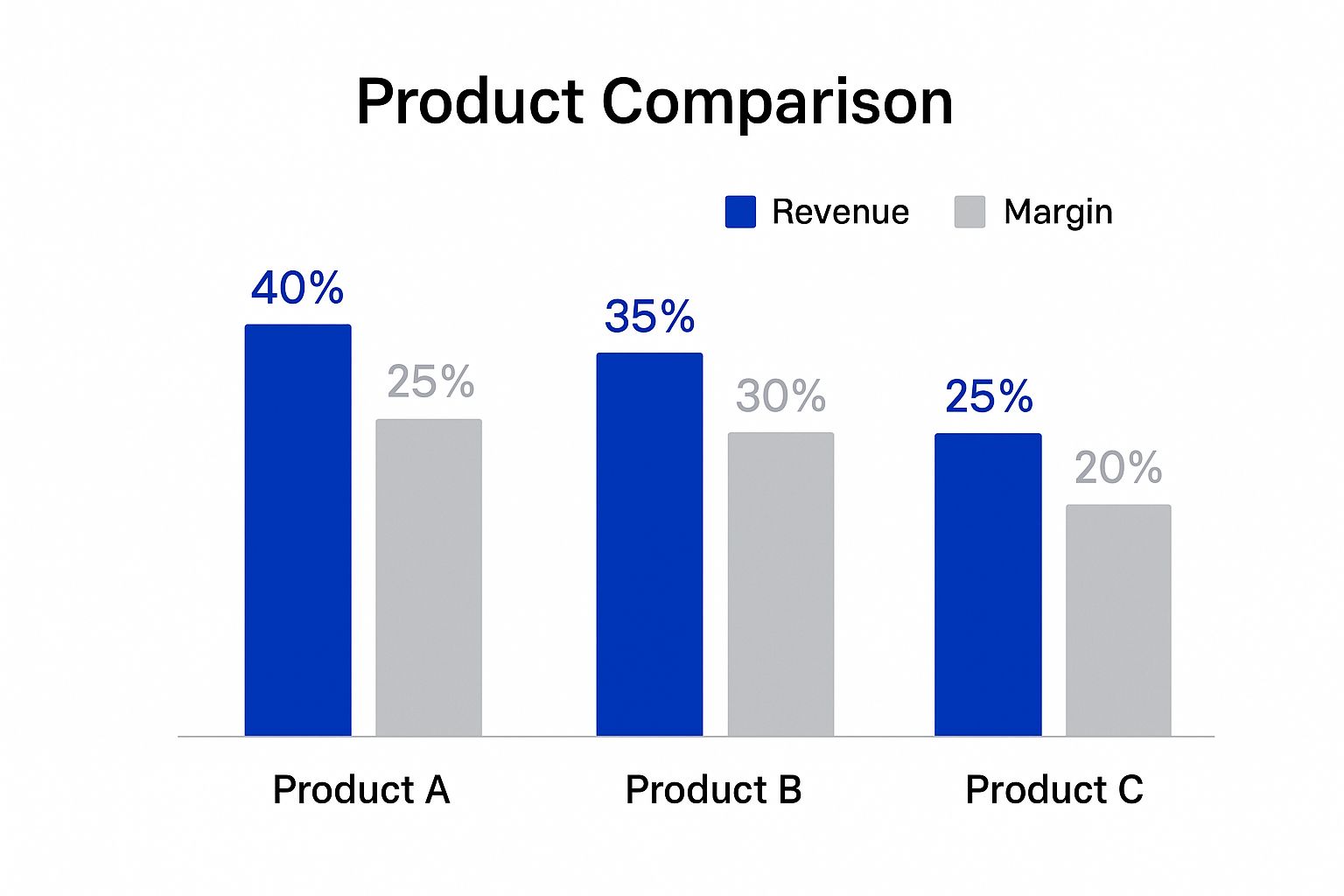

A classic mistake I see is businesses focusing only on their highest-revenue products without digging into their actual profitability. This chart shows it perfectly: the product bringing in the most cash isn't always the one that's best for your bottom line.

Here, Product B might generate less total revenue than Product A, but it contributes more profit. That makes it a much more efficient use of your capital and warehouse space.

My Take on Supply Chains

From my experience, optimising your supply chain is about so much more than just finding the cheapest supplier. It’s about building rock-solid partnerships, shrinking lead times, and guaranteeing quality to slash costly returns and delays. That’s where the real value is.

You could look at implementing a just-in-time (JIT) inventory system, where you only order materials as and when you need them for production. It’s a brilliant way to cut down on storage costs and waste. Many businesses are also seeing great results by leveraging 3PL services for profitability, essentially outsourcing the headaches of warehousing and distribution.

To pinpoint where you can make the biggest impact, it helps to map out your current processes.

Finding Your Biggest Efficiency Wins

A look at common operational hurdles and the practical solutions you can implement to boost productivity and cut down on waste.

Taking a systematic look like this often reveals surprisingly simple fixes that can have a massive cumulative effect on your profit margins.

Invest in Your Team’s Skills

At the end of the day, your single greatest asset in the hunt for efficiency is your team. A skilled, motivated, and empowered team will naturally find better ways of doing things. Pouring resources into training and development isn't an expense; it's a direct investment in your company's operational strength.

When your people understand the "why" behind their work and have the right tools and skills, they become more engaged and far more productive.

Here are a few practical ways to do this:

- Cross-Training: Train people in a few different roles. This builds a more agile workforce that can cover for absences and adapt to shifting priorities without missing a beat.

- Process Improvement Training: Teach your team the basics of lean management or continuous improvement. Give them the power to spot and fix bottlenecks in their own daily workflows.

- Tech Upskilling: Make sure everyone is confident and proficient with the software you use. Proper training often uncovers time-saving features that people never knew existed.

By building a culture of continuous improvement, you make efficiency a core part of how your business thinks and acts, not just a one-off project. If you're keen to dig deeper, our guide on improving operational efficiency offers more ideas for creating a truly productive workplace. This proactive mindset is what ensures your operations are always working to build a healthier bottom line.

Fine-Tuning Your Product and Customer Mix

It’s a tough lesson to learn, but not all revenue is good revenue. Some of your products, some of your services, and yes, even some of your customers are dramatically more profitable than others. The secret to a healthier profit margin often lies in directing your energy and resources to the parts of your business that deliver the biggest bang for your buck, rather than spreading yourself too thin.

This is all about getting strategic with what you sell and who you sell it to. Once you can pinpoint your star performers, you can double down on what’s working. At the same time, you can start making some tough but necessary decisions about the resource-heavy parts of your business that are quietly draining your profits.

Applying the 80/20 Rule to Your Sales

You’ve probably heard of the Pareto principle, or the 80/20 rule. It’s a game-changer when you apply it to your business. The principle suggests that around 80% of your profits come from just 20% of your products or customers. Your first job is to find that vital 20%.

Start by digging into your sales data from the past year. Don't just glance at the top-line revenue numbers; you need to get granular and calculate the gross profit for each specific product or service you offer.

The results might genuinely surprise you. I once worked with a web design agency that discovered something fascinating. Their big, custom website builds looked great on paper, bringing in huge revenue figures. But the profit margins were razor-thin after factoring in all the project management and endless revisions. Their real money-maker? Smaller, standardised SEO packages. They brought in less revenue per project, but the margins were fantastic, making them the true profit engine of the company.

With that kind of clarity, you can take decisive action:

- Shine a Spotlight on Your Stars: Your high-profit, popular items need to be the heroes of your marketing campaigns. Put them front and centre.

- Deal with the Duds: For low-profit items, you have a few options. Can you raise the price? Can you find a way to reduce the cost to deliver? Or is it simply time to cut it loose and discontinue the offer?

Pinpointing Your Most Valuable Customers

Just like your products, a small group of your customers is likely driving the lion's share of your profit. Nurturing these relationships is far more efficient and cost-effective than constantly being on the hunt for new leads. The metric you need to get to grips with here is Customer Lifetime Value (CLV).

CLV is a forecast of the total profit your business can expect from a single customer over the entire course of your relationship. It’s a powerful lens that shifts your focus from the first transaction to the long-term value of loyalty and repeat business.

A customer with a high CLV isn't just someone who buys from you again and again; they’re often the ones who buy your most profitable services. These are your VIPs, and they deserve to be treated as such.

When you know who your top-tier customers are, you can build retention strategies specifically for them. A surprise discount, exclusive access to a new service, or even just a personal phone call to check in can work wonders for strengthening these critical relationships and locking in future profits.

Analysing your customer data helps you build a detailed profile of your ideal, high-CLV client. Once you understand their industry, company size, and the specific challenges they face, you can fine-tune your marketing to attract more people just like them.

Growing Revenue with Upselling and Cross-Selling

Once you've identified your best customers—the people who are already happy and see the value in what you do—you have a golden opportunity. You can grow your revenue without the hefty price tag of acquiring a brand-new customer. This is where upselling and cross-selling come in.

- Upselling is simply about encouraging a customer to buy a more premium version of a product or service. A classic example is a software company offering a 'Pro' plan with advanced features.

- Cross-selling is about suggesting a related or complementary product. An accounting firm, for instance, might offer financial advisory services to an existing bookkeeping client.

The real art to both is making sure your timing and relevance are spot on. Your offer should feel like a genuinely helpful suggestion that solves another one of your customer’s problems, not a sleazy sales pitch. For example, after you’ve successfully wrapped up a project, you could send a follow-up email with a case study showing how a similar client achieved even greater results by adding another one of your services.

By shifting some of your sales focus from pure acquisition to expansion, you're tapping into a warm, receptive audience. It's a remarkably efficient way to give your overall profit margins a healthy boost and build a more resilient business for the long haul.

Got Questions About Improving Your Profit Margins?

If you're trying to get your business into better financial shape, you're not alone. I've found that most business owners, whether they're old hands at this or just starting out, tend to hit the same walls and ask the same questions. Let's tackle some of the most common ones.

What Is a Good Profit Margin for a Small Business?

This is the big one, but the honest answer is always: it depends entirely on your industry. A "good" profit margin for a software company would be a complete disaster for a high-street coffee shop. Context is everything.

For example, a restaurant in the UK might be thrilled to hit a net profit margin between 2% and 6% – the margins are just that tight. Meanwhile, a digital marketing agency or a business consultant could be aiming for 20% or more, simply because their overheads and cost of goods sold are so much lower.

The real trick isn't to chase some magic number. It's to benchmark your performance against businesses like yours, in your specific niche. Your main goal should always be to improve on your own past performance, quarter after quarter.

How Quickly Can I Actually Improve My Margins?

How fast you'll see a change really depends on what levers you decide to pull. Some tweaks can deliver an almost instant boost, while others are more of a long game – an investment in your company's future financial health.

Here’s a rough idea of what to expect:

- Quick Wins (A Few Weeks): Things like adjusting your pricing, especially on your best-selling items, can lift your gross margins from the very next sale. Another quick fix is doing a full audit of your software subscriptions – you’d be amazed how many ‘zombie’ accounts you can cut and see savings in the next billing cycle.

- Medium-Term Gains (A Few Months): Renegotiating contracts with your main suppliers or rolling out a new piece of software to make your team more efficient usually takes a couple of months to really show up on the bottom line. It’s a bit of upfront effort for a consistent, recurring payoff.

- Long-Term Impact (6+ Months): Bigger, more strategic moves like investing in team training or fundamentally changing your product mix take time. The results can be huge, but they build up gradually as your team gets up to speed and new sales patterns take hold.

Should I Focus on Cutting Costs or Increasing Prices?

Honestly? The best strategy is a bit of both. But to figure out where to start, you need to look at your profit and loss statement. Where’s the biggest opportunity hiding in plain sight?

If your gross profit margin looks healthy but your net profit margin is getting squeezed, that's a massive red flag that your operating costs are out of control. In that case, your first move should be a ruthless hunt for savings and operational tweaks. You're making good money on each sale, but it's all being eaten up by overheads before it hits your pocket.

On the other hand, if your gross margin is thin, you’re not making enough profit on the things you actually sell. Pricing is your most powerful tool here. You need to look at value-based pricing, maybe introduce tiered options, or even have the tough conversation about dropping your least profitable services. Trying to just trim costs won't fix a problem that's rooted in your pricing.

Will Raising Prices Drive My Customers Away?

It’s a fair question and a common fear, but I’ve found it’s usually overblown. The secret is to handle price increases with a bit of strategy and to be really clear about the value you provide. A sudden, unexplained price hike will almost certainly annoy people. A well-justified one? Most loyal customers will get it.

Before you touch your prices, think about this:

- Start Small: Test the waters with a modest increase on just one product line or a single service tier. See what happens. Watch the data closely before you think about a wider rollout.

- Add More Value: Don't just increase the price. Bundle it with something extra – a new feature, a better service level, or a noticeable quality improvement. This changes the conversation from "you're charging me more" to "I'm getting more for my money."

- Talk to People: For your existing clients, give them a decent amount of notice. Explain why the price is changing. Maybe your material costs have shot up, or you're investing in better tech to serve them. Frame it as a necessary step to maintain the quality they expect, not just to line your pockets.