Boosting your profit margins isn't simply about chasing more sales. The real art lies in keeping a larger slice of the revenue you generate. I've found that the most effective approach is a two-pronged attack: systematically cutting your costs while, at the same time, strategically optimising your prices and revenue streams. It means taking a magnifying glass to every expense and making sure each pound is pulling its weight.

Establishing Your Profitability Baseline

Before you can even think about improving your margins, you need a completely honest picture of where your business is right now. Think of it like a road trip – you can’t map out the route until you know your exact starting location. This initial financial health check is the single most important first step.

To do this properly, you need to get comfortable with your numbers and master data analysis and business intelligence. This goes way beyond a quick glance at the bottom line of your P&L statement. It’s about breaking down that final profit figure into its core components.

Understanding Your Core Margin Metrics

Each profit margin metric tells you a different part of your business's story. By calculating all three, you get a 360-degree view of your financial health, from the cost of making your product all the way to the final profit.

To make this easier, here's a quick guide to the three formulas you absolutely need to know.

Your Quick Guide to Profit Margin Formulas

Understanding these isn't just an accounting exercise; it's the key to diagnosing where your business is strong and where it's bleeding cash.

Setting Realistic Benchmarks

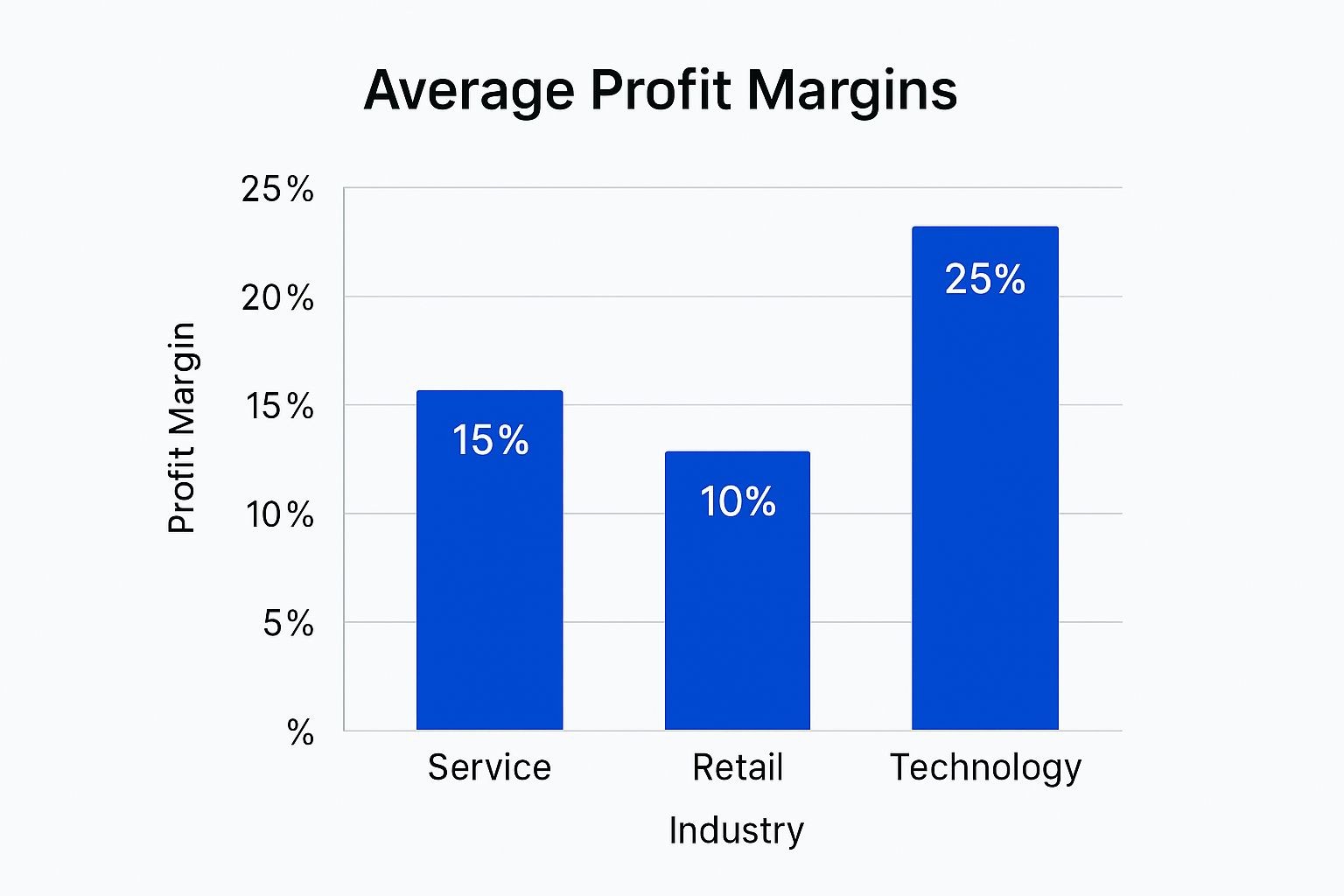

So, you've got your numbers. The next question is, are they any good? This is where industry benchmarks are essential. A 15% net profit margin might be fantastic for a UK retailer, but it would be a serious cause for concern in a software company.

For example, when you look at gross margins across the UK, the differences are stark. A Software-as-a-Service (SaaS) business might enjoy margins of 75% to 85%. In contrast, a retail e-commerce store is more likely to be in the 30% to 45% range. The hospitality sector? They often operate on even tighter margins, sometimes as low as 20%.

The chart below shows just how much these averages can vary between major sectors.

It’s clear that a tech business, for instance, has a very different profitability ceiling than a service or retail operation. That’s why comparing your performance against your direct industry peers is so important. Once you have this clear, data-driven baseline, you can start setting goals for growth that are both ambitious and achievable.

Uncovering the Hidden Costs Bleeding Your Business Dry

Real profitability isn't just about revenue. It's about what you actually keep. If you're serious about boosting your profit margins, you need to put on your detective hat and hunt down the hidden costs that are quietly eating away at your bottom line. More often than not, these culprits are lurking in your Cost of Goods Sold (COGS) and Operating Expenses (OpEx).

It's easy to think you have a solid handle on your spending. But I've seen it time and again: small, seemingly insignificant inefficiencies snowball into a massive drain on resources. We’re talking about everything from outdated supplier contracts and dusty excess stock to that software subscription you forgot you were even paying for. The first, most crucial step is to start questioning every single expense.

Diving Deep into Your Direct Costs

Let's start with your direct costs—the expenses directly tied to making your product or delivering your service. This is often the best place to find savings that go straight to your gross profit margin.

Begin by putting your supplier relationships under the microscope. Are you truly getting the best price for your raw materials or components?

A classic mistake I see businesses make is letting supplier agreements roll over year after year without a second thought. Markets shift, new vendors pop up, and your own buying power might have increased significantly. Don't be shy about renegotiating or seeing what else is out there.

If you deal with physical products, your inventory management is another goldmine. Every single item on your shelves has a carrying cost tied to it—storage, insurance, and the risk of it becoming obsolete. A small manufacturing client of mine, for example, realised they could slash material waste by 15% just by fine-tuning their cutting processes. That was a direct, immediate boost to their profit on every unit they sold.

Trimming Your Operational Overheads

Next up are your operating expenses, the costs needed just to keep the lights on, separate from production. This category is famous for "expense creep," where tiny, non-essential costs build up over time without anyone noticing. A full-scale audit here is non-negotiable.

Your mission is to categorise every single operating expense and examine it with a critical eye.

- Software & Subscriptions: Are you paying for tools your team ditched months ago? You’d be surprised how many companies are paying for redundant software licences that can be cancelled today.

- Utilities & Rent: These might feel fixed, but there's often wiggle room. Simple, energy-efficient upgrades can make a real dent in your utility bills over time.

- Marketing & Advertising: Dig into the return on investment (ROI) for every marketing channel. Are you throwing good money after bad on campaigns that aren't delivering results? Shift that budget to what actually works.

This isn't about slashing costs indiscriminately; it's about making smart, strategic choices. For a more detailed breakdown, our guide on how to reduce operating costs offers practical tips without stunting your growth. By systematically finding and plugging these financial leaks, you build a leaner, more resilient, and far more profitable business.

Rethinking Your Pricing for Maximum Value

Once you’ve got a firm handle on your expenses, the next obvious place to look for profit is your price tag. It’s amazing how many UK businesses get stuck in the "cost-plus" rut. They work out their costs, tack on a standard percentage, and that’s that. While this feels like a safe, logical approach, you’re almost certainly leaving cash on the table.

To really move the needle on profit, you need to shift your mindset towards value-based pricing. This is a complete reframe. You stop thinking about what your service costs you and start focusing on the value it delivers to your customer. It takes more research and a genuine understanding of your market, but the rewards are significant. Think about it: a specialist software developer doesn't bill just for the hours they spent coding. They charge based on the massive efficiency gains or cost savings their solution unlocks for the client.

Moving Beyond Simple Competitor Copying

So, where do you start? Many people’s first instinct is to see what the competition is charging. While that’s good for getting a feel for the market, it should never be your entire strategy. Blindly matching or undercutting a rival is risky—it assumes their pricing is smart and their cost base is identical to yours. Both are big gambles.

Instead, use competitor pricing to map out the landscape and figure out where you sit. Are you the premium, white-glove service? Or are you the go-to, budget-friendly option? Your position here is everything. A high-end artisan bakery in Chelsea isn't competing with a supermarket loaf, and its pricing needs to reflect that. They’re selling a completely different experience, a higher quality product, and a sense of exclusivity.

Implementing More Sophisticated Pricing Tactics

When you’re confident in the value you offer, you can start getting more creative with how you present your prices. Two of the most effective strategies I’ve seen for boosting average order value are tiered pricing and product bundling.

Tiered Pricing: This is the classic "Good, Better, Best" model. By offering a few distinct packages, you guide customers' choices. The middle option often looks like the most sensible deal, encouraging people to spend a bit more than they might have otherwise. A car wash is a perfect example: a basic wash, a wash and wax, and a full valet service.

Product Bundling: This one’s simple but powerful. Group a few related items together and offer them for a single, attractive price. A local coffee shop might sell a latte for £3.50, but bundle it with a pastry for £5.00. That small nudge increases the total sale and helps them sell more pastries.

One of the biggest takeaways from behavioural economics is that pricing is all about perception. It’s not just a numbers game. Small tweaks, like pricing something at £19.99 instead of £20.00, can make a surprising difference. This is often called charm pricing, and it works because of how our brains process numbers.

Ultimately, pricing is a dynamic part of your business, not something you set and forget. Your goal is to find that sweet spot where the customer feels they’ve received fantastic value and your business is capturing a healthy return. It requires testing, listening to feedback, and being brave enough to adjust your prices to reflect your true worth.

Driving Efficiency in Your Daily Operations

Beyond simply crunching numbers on costs or prices, one of the biggest wins for your profit margin is hiding in plain sight: your daily workflow. Those small, repetitive, and often invisible hiccups in your operations—what I call 'operational drag'—are silent profit killers. It's the extra hour spent on manual data entry, the lag from a miscommunication between teams, or that stubborn bottleneck in your service delivery.

Individually, they seem minor. Collectively, they drain your time, money, and momentum.

To get a grip on this, you need to stop seeing your business as a collection of separate tasks and start viewing it as a single, interconnected system. The real goal is to make that system hum, getting more done with less effort and waste.

Mapping Your Processes to Find Bottlenecks

You can't fix a problem you don't fully understand. The first step is to get visual. Grab a whiteboard or even just a large piece of paper and map out a core business process from the very beginning to the very end. This could be anything from how you fulfil a customer order to how you onboard a new client.

As you chart the course, be a detective. Ask tough questions at every single stage:

- Where does one person hand a task off to another? Is it seamless?

- Which steps consistently seem to take the longest?

- What tasks are mind-numbingly repetitive and prone to simple human error?

I guarantee this exercise will uncover some surprises. I once worked with a small e-commerce business that was losing a full 24 hours on order fulfilment. Why? Because two different software systems weren't talking to each other, forcing a team member to spend their morning manually re-entering data. A single integration fix saved them countless hours and immediately boosted customer satisfaction.

A crucial part of this is being brutally honest with yourself. It's incredibly easy to fall into the "that's how we've always done it" trap. You have to challenge those assumptions and be ready to find the flaws. Real operational improvement starts the moment you acknowledge where the friction truly lies.

Bringing in Technology and Specialised Talent

Once you’ve pinpointed the weak spots, you can start bringing in solutions. Technology is your best friend here. Automation software can take over the tedious work—invoicing, data entry, scheduling—freeing up your team to focus on the high-value activities that actually grow the business.

This is particularly relevant when you look at how profitability varies across UK SMEs. For example, sectors like property and business services average a profit of around £15,000, while retail and manufacturing are often closer to £11,000. Much of that difference comes down to who is running a tighter ship operationally.

Another powerful strategy is to integrate specialised remote talent. Instead of taking on the full cost and commitment of an in-house digital marketer or financial analyst, you can access world-class skills on a flexible basis. Services like Beyond Hire connect businesses with vetted professionals who can manage specific functions, giving you immediate expertise without the heavy overheads of a full-time salary.

For more hands-on advice, check out this excellent resource on How to Streamline Business Processes for Efficiency. You can also find more of our own insights on how to streamline business processes in our detailed guide. By pairing smart tech with the right expertise, you build a lean, agile operation that's truly designed for profit.

Growing Revenue from Your Existing Customers

While getting your costs and pricing right is absolutely vital, that's only half the battle. The other, and frankly more exciting, part of the profit puzzle is boosting your revenue. But this doesn't have to mean a frantic, expensive scramble for new clients. Often, the biggest opportunities are sitting right under your nose, within your existing customer base.

Think about it this way: attracting a brand-new customer can cost anywhere from five to twenty-five times more than keeping one you already have. That’s a massive difference. It highlights a simple truth I've seen play out time and time again: your current customers already get what you do, they trust you, and they're far more likely to buy from you again. You just need to give them a good reason.

Turning One-Time Buyers into Repeat Business

The most direct way to get more from your existing customers is through upselling and cross-selling. This isn't about aggressive sales tactics; it's about being genuinely helpful and anticipating what they'll need next.

- Upselling: This is where you encourage a customer to go for a slightly better, more premium version of what they're already buying. Imagine a web hosting company seeing a client's e-commerce site is growing fast. Offering them an upgraded package with more storage and beefed-up security isn't just a sale—it's good service.

- Cross-selling: This involves suggesting products that complement what they've just bought. If someone buys a new laptop from you, offering a discount on a protective case or a wireless mouse is a natural fit. It just makes sense.

To pull this off, you have to get familiar with your customer data. Dive into their purchase histories and look for patterns. What products do people often buy together? If someone bought a particular item six months ago, what's their next logical step? When you use data this way, your offers feel like smart recommendations, not just another sales pitch.

Building Lasting Loyalty and Advocacy

Beyond just the next sale, the real long-term win is maximising Customer Lifetime Value (CLV). This is a fancy term for a simple idea: the total amount of money you can expect to make from a single customer over the entire course of your relationship. A high CLV gives your business a much more stable and predictable flow of income.

The most profitable customer isn't the one who makes the single biggest purchase. It's the one who keeps coming back. They become a reliable source of income, which in turn drives down what you need to spend finding new business in the future.

Putting a simple loyalty programme in place is a brilliant way to increase CLV. It doesn’t have to be complicated. The local coffee shop’s "buy nine, get your tenth free" card is a classic for a reason—it works. If you're a service-based business, maybe you offer a discount on a client's next project or give them early-bird access to new services.

Ultimately, your goal is to turn happy customers into brand advocates. When someone is so pleased with your work that they recommend you to their friends and colleagues, they’re doing your marketing for you—at no cost. This powerful mix of repeat business and word-of-mouth promotion is a double victory. You're driving revenue up while you simultaneously work to cut business expenses. It's this two-pronged approach that truly builds a sustainable, profitable business.

Your Top Profit Margin Questions, Answered

When you're running a business, the numbers can feel overwhelming. Questions like "Is my profit margin any good?" or "Where on earth do I even start cutting costs?" are constantly buzzing around. Let's tackle some of the most common questions UK business owners face and give you some straight, practical answers.

This isn't about dry accounting theory. It's about real-world moves you can make that will genuinely fatten up your bottom line.

What Is a Good Profit Margin in the UK?

There's no magic number here. A "good" profit margin is completely different from one industry to the next.

A 5% net profit margin might be fantastic for a supermarket shifting huge volumes, but it would be a major red flag for a bespoke software development agency. The real question you should be asking is, "What's a good profit margin for my specific industry?"

Your mission is to find your industry's average and then aim to beat it. For context, here are a few ballpark figures:

- Retail: Often operates on very thin margins, typically between 2-6%.

- Restaurants & Hospitality: With high overheads like rent and staff, average net margins can hover around 3-7%.

- Software/SaaS: This is where you see the big numbers. Thanks to low costs per additional customer, margins can easily top 20-30%.

Do your homework, find the benchmark for your sector, and set your sights on landing in the top quarter.

Which Costs Have the Biggest Impact on Profit?

For almost every business, the two biggest profit eaters are the Cost of Goods Sold (COGS) and labour expenses.

It’s a classic case of the 80/20 rule. I’ve found that focusing on the top 20% of your expenses—the big-ticket items—is where you’ll find 80% of your potential savings. If you’re a manufacturer, that's your raw materials. If you're a service business like mine, it's almost always your payroll.

Start by digging deep into these major cost centres. Shaving a few percentage points off your biggest expenses will have a much more significant impact than scrimping on office supplies. If you're looking for a wider view on financial health, it’s worth exploring some proven strategies for saving money in business.

How Can I Increase Profits Without Just Raising Prices?

Hiking up prices is the most obvious way to increase profit, but it’s a blunt instrument that can easily scare off customers. A much smarter approach is to focus on increasing your Average Transaction Value (ATV) and Customer Lifetime Value (CLV). In simple terms, get each customer to spend more with you, more often.

This is where you can get creative. Try tactics like:

- Product Bundling: Group complementary products together at an attractive price. Think a camera, lens, and memory card sold as a single kit.

- Upselling: Offer a slightly better, more premium version of what the customer is already buying.

- Cross-selling: Suggest related items at checkout. "Customers who bought this also bought..." is a classic for a reason.

These methods boost how much you make from each sale without the backlash of a sudden price increase. The timing couldn't be better, either. The wider economic picture shows that UK corporate profits hit an impressive £152.043 billion in the first quarter of 2025, marking a continued upward trend. You can find out more about UK corporate profitability trends here. This shows there's plenty of opportunity out there for businesses ready to get sharp on their strategy.